How Proposed Bank Capital Rules Could Deliver Strategic Benefits for Banks

Federal banking agencies recently proposed significant updates to bank capital rules. We view these adjustments as highly favorable.

However, leaders must carefully evaluate the specific details of these regulations before moving forward. Making the proper election allows your institution to:

- Boost risk-based capital levels

- Gain additional operational flexibility

What Proposed Bank Capital Rule Changes Mean for Banks

The proposal primarily focuses on changes to risk weightings, treatment of off-balance sheet commitments, removing the mortgage servicing asset (MSA) deduction threshold, and recognition of accumulated other comprehensive income or loss (AOCI) in CET1.

Generally, three primary capital frameworks may apply, depending on eligibility and elections:

- Community Bank Leverage Ratio (CBLR)

The proposed standards also include the following general changes to capital treatment:

- Eliminate the requirement to deduct MSAs above a threshold (25% of CET1 under current rules) from common equity Tier 1 capital for all covered banking organizations.

- Require Category III and IV banking organizations to recognize certain elements of AOCI in common equity Tier 1 capital.

Proposed Capital Rule Adjustments

The 2026 proposed capital rules introduce substantial adjustments for regulated banking institutions. These updates modify the treatment of Mortgage Servicing Assets and Accumulated Other Comprehensive Income while maintaining existing frameworks for subordinated debt.

Changes to Mortgage Servicing Assets

The proposal eliminates deduction thresholds for Mortgage Servicing Assets (MSAs) and subjects all MSAs to a uniform 250 percent risk weight.

- Current rule: Covered banking organizations must deduct the amount of MSAs that exceed 25 percent of common equity tier 1 capital.

- Proposed impact: The changes remove the numerator impact, affecting only the denominator.

- Strategic outcome: Removing the previous structural cap creates increased flexibility to hold these assets on the balance sheets of regulated banking institutions.

New Requirements for Accumulated Other Comprehensive Income

The rules mandate Category III and Category IV banking organizations to include most components of Accumulated Other Comprehensive Income (AOCI) in common equity tier 1 capital.

- Alignment: This change aligns the treatment of these organizations with Category I and Category II institutions.

- Exclusions: The requirement excludes gains and losses on cash-flow hedges when the organization does not recognize the hedged item on the balance sheet at fair value.

- Implementation timeline: The proposal establishes a five-year phase-in period from 2027 through 2031. Organizations will fully reflect AOCI in capital by 2032.

Community Bank Leverage Ratio

The Community Bank Leverage Ratio (CBLR) framework delivers a streamlined alternative to complex capital requirements for qualifying institutions. Eligible banking organizations must weigh lower required capital under the standard risk-based framework against the simpler reporting requirements of the CBLR framework.

Eligibility Requirements

The initial CBLR applied to banks with under $10 billion in consolidated assets. Institutions must meet specific criteria to qualify, which include:

- Operating as a non-advanced approaches banking organization.

- Maintaining off-balance sheet exposures and commitments under 25% of consolidated assets.

- Holding trading assets and trading liabilities under 5% of consolidated assets.

Capital Thresholds & Compliance

Regulators set the minimum ratio at 9% for 2025. A finalized rule decreases this threshold to 8%, effective July 1, 2026. Regulators classify banks electing the CBLR framework as well-capitalized if they maintain the 8% minimum threshold starting in the third quarter of 2026.

Regulatory Interactions

Regulatory agencies note limited interactions between the Standardized Approach, the Expanded Risk-Based Approach (ERBA) proposal, and the CBLR framework. Depository institutions that adopt the CBLR framework automatically meet the minimum risk-based capital requirements and achieve well-capitalized status.

Non-CBLR Under Basel III Endgame Proposal

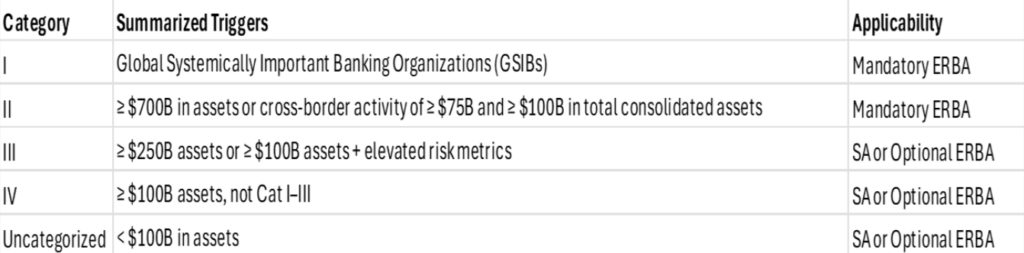

The Standardized Approach and Expanded Risk-Based Approach (ERBA) are delineated based on asset size and other triggers based on the Category definitions as summarized below:

The ERBA establishes clear requirements for credit risk, equity risk, and operational risk, alongside a revised market risk framework. Notably, ERBA is an optional election for banks of all sizes, extending beyond Category I and Category II institutions. This provides qualifying banks the strategic option to adopt the framework and leverage the new rules to their advantage. Electing ERBA can substantially increase risk-based capital levels, depending on portfolio composition.

As noted in the proposal:

“the agencies expect the proposal to reduce the common equity tier 1 capital requirements applicable to Category III and IV holding companies by 3.0 percent and the capital requirements applicable to smaller holding companies (i.e. holding companies with total assets under $100 billion that report risk-based capital on FR Y-9C) by 7.8 percent. The reduction in requirements for Category III and IV holding companies reflects a 6.1 percent reduction due to the revised risk-weighted assets combined with an estimated 3.1 percent increase in capital requirements due to an estimated long-run average impact of including AOCI in regulatory capital. Similarly, the agencies expect the proposal to reduce the common equity tier 1 capital requirements applicable to depository institution subsidiaries of Category III and IV banking organizations by 4.7 percent, and those applicable to smaller depository institutions by 8.0 percent.”

The Standardized Approach

The Standardized Approach applies to banks outside the Community Bank Leverage Ratio framework and those exempt from the Expanded Risk-Based Approach. Under the new rules, any bank may adopt the ERBA.

The proposal introduces targeted adjustments to risk weights to reflect a more risk-sensitive treatment. Primary changes include:

- Reducing the corporate exposure risk weight from 100 percent to 95 percent.

- Lowering the risk weight for all assets not specifically assigned a different category from 100 percent to 90 percent.

- Implementing a broader, more granular range of risk weights for residential mortgage exposures.

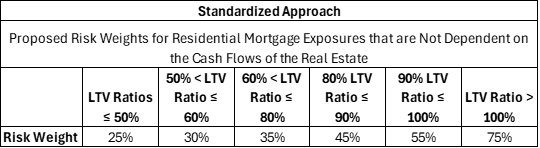

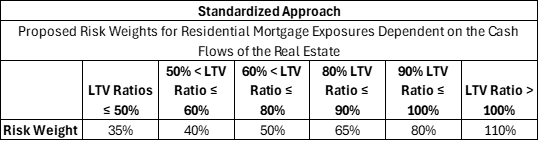

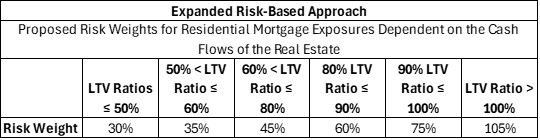

Residential Mortgage Exposures

The proposed guidance retains the current definitions of residential mortgage exposures. It introduces a risk-sensitive framework that assigns risk weightings based on loan-to-value (LTV) ratios. Mortgages dependent on property cash flows, particularly non-owner-occupied properties, receive higher risk weights. The LTV-based approach applies only to prudently underwritten, performing loans. All other loans default to a 100% risk weight.

To use the LTV approach, residential mortgage exposures must meet four criteria:

- Secured by an owner-occupied or rented property.

- Underwritten according to prudent standards, including the loan amount as a percentage of the property value.

- Current on payments, avoiding nonaccrual status or being 90 days or more past due.

- Unmodified and unrestructured.

The proposal assigns risk weights to residential mortgage exposures based on LTV ratios and property cash flow dependency. This creates a dynamic, risk-sensitive framework where capital requirements decline as borrowers build equity.

Compared to the current standardized approach, the proposal improves alignment with underlying credit risk by incorporating borrower equity and repayment structure. It maintains transparency and consistency across institutions. The proposed tables are as follows:

The proposal reduces standard approach risk weights to align with observed credit and operational risks while maintaining a straightforward approach. The expanded risk-based framework drives these revisions, integrating credit risk and a simplified operational risk add-on without introducing additional complexity.

Key adjustments include:

- Corporate exposures decrease from 100% to 95%.

- Other assets decrease from 100% to 90%.

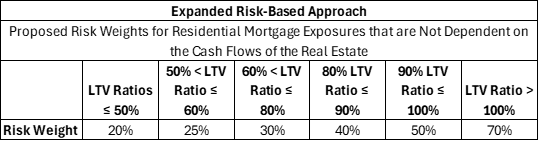

Expanded Risk-Based Approach (ERBA)

Any institution can elect the ERBA, although it targets Category I and Category II institutions. The framework offers favorable treatments for residential exposures and details more granular corporate exposures, including commercial real estate, consumer and industrial, and farm loans. These granular exposures apply to entities not explicitly defined under the current rule set, as outlined below:

Residential Mortgage Exposures

Corporate Exposures

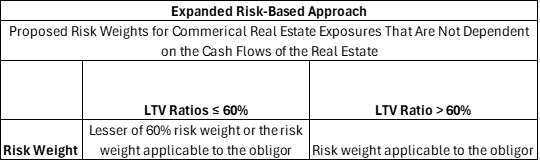

The proposal extends the LTV‑based and cash‑flow dependency framework used for residential real estate to commercial real estate exposures. It assigns risk weights based on both borrower equity and the source of repayment.

For exposures that are not dependent on property cash flows, risk weights are primarily driven by the obligor’s creditworthiness. However, if the bank lacks sufficient information and the LTV exceeds 60%, a 100% risk weight applies (unless the exposure is nonperforming).

The general tables are outlined below:

Corporate exposures can also fall under small to medium sized entity classifications as noted below in the Retail Exposures section.

Acquisition, Development, or Construction (ADC) Exposures

The proposal defines ADC exposures broadly as real estate loans for acquisition, development, or construction, assigning a 100% risk weight unless the exposure qualifies as HVCRE (which receives a 150% risk weight) or is nonperforming. Unlike other real estate exposures, ADC treatment does not depend on LTV or cash‑flow characteristics, reflecting their inherently higher, short‑term development risk.

The proposal categorizes real estate loans for acquisition, development, or construction as ADC exposures. These exposures carry specific risk weights based on their classification.

- Standard ADC Exposures: Receive a 100% risk weight.

- HVCRE Exposures: Receive a 150% risk weight.

- Nonperforming Exposures: Subject to standard nonperforming classifications.

Unlike other real estate loans, ADC treatment ignores LTV ratios and cash-flow characteristics. This direct approach reflects the inherently higher short-term risk of development projects.

Other Real Estate Exposures

The proposal establishes a distinct classification for exposures that fall outside standard commercial, residential, or ADC real estate definitions. This framework addresses transaction risks by assigning specific risk weights based on cash flow dependency and underwriting strength.

Key classifications include:

- Default 150% risk weight: This applies to non-standard, speculative, or cash-flow-dependent transactions to account for their elevated risk profile.

- Standard 100% risk weight: Certain residential exposures that do not rely on property cash flows, such as junior liens or loans with relaxed underwriting standards, receive this weight.

These thresholds clearly define the risk associated with subordinated claims. They also reinforce the necessity of strict underwriting practices to qualify for more favorable capital treatment.

Retail Exposures

The proposal introduces a revised definition of retail exposure. It includes non-real estate exposures to individuals and small or medium-sized entities (SMEs). The update assigns specific risk weights based on product type, borrower characteristics, repayment behavior, and portfolio diversification.

Key risk weight applications include:

- Regulatory Retail Exposures: Eligible exposures up to $1 million per obligor receive a 45% risk weight for transactors and a 75% risk weight for non-transactors.

- Other Retail Exposures: The rule treats larger or non-qualifying SME exposures more conservatively, assigning them a 100% risk weight or classifying them as corporate exposures.

Evaluating Potential Framework Elections

There are additional classifications, requirements, and guidelines outside this scope. These include derivative instruments and off-balance sheet exposures/commitments, both of which carry significant capital implications. Furthermore, the Expanded Risk-Based Approach introduces substantial calculations and complexity across thousands of pages.

Banks should evaluate potential framework elections before the final rule issuance. These changes are significant. Maximizing your institution’s capital capacity requires thoughtful analysis and planning.

The Standardized Approach and Expanded Risk-Based Approach will likely benefit banks with significant mortgage servicing assets, higher concentrations in residential or commercial real estate lending, strong underwriting, and expectations for considerable balance sheet growth. Consider the following framework trade-offs:

- The Community Bank Leverage Ratio: Provides simplicity and a lower reporting burden with less flexibility.

- The Standardized Approach: Offers greater flexibility with moderate added complexity.

- The Expanded Risk-Based Approach: May offer the greatest capital benefit alongside increased operational and modeling complexity.

Early modeling and scenario analysis are critical to determine the optimal framework and position your institution for future growth. Contact our team today to learn more.